There is no point in living a life where you’ve overspent all your money and still have no money left because you can’t expect that you’ll have a surplus later. Money troubles can be scary, but they don’t have to wreck your life. We’ll show you how to fix a failing budget and get on the road to financial freedom in this blog.

All you need to know about budgeting is that it’s a process of spending less than you earn. For the most part, you can do this just by taking one paycheck off the table. But if you’re like most people, you do it by looking at your budget every month and making cuts. So if you’re not getting exactly what you want, you have to know how to fix it.

Create a Plan for Managing Your Money Before it Manages You

The truth is, budgets aren’t easy to make. You have to plan out your purchases, set allowances for regular purchases, and pay attention to your money. You also have to make sure you’re not spending too much, that your income is sufficient, and that you’re saving towards achieving your financial goals. If you take all of that into consideration, you’ll be able to create a budget that works for you.

Find Where Your Money Is Going

As you make budgeting a yearly exercise, you’ll notice that you’re careful with money. You know there’s a need to live within your means, and you want to know which expenses are truly necessary and which are just a waste of money. But you’re not always sure you’re doing the right thing. Take a look at the money you spend and see if you really need to spend it. Find out where the money is going and how you can cut it out of your budget.

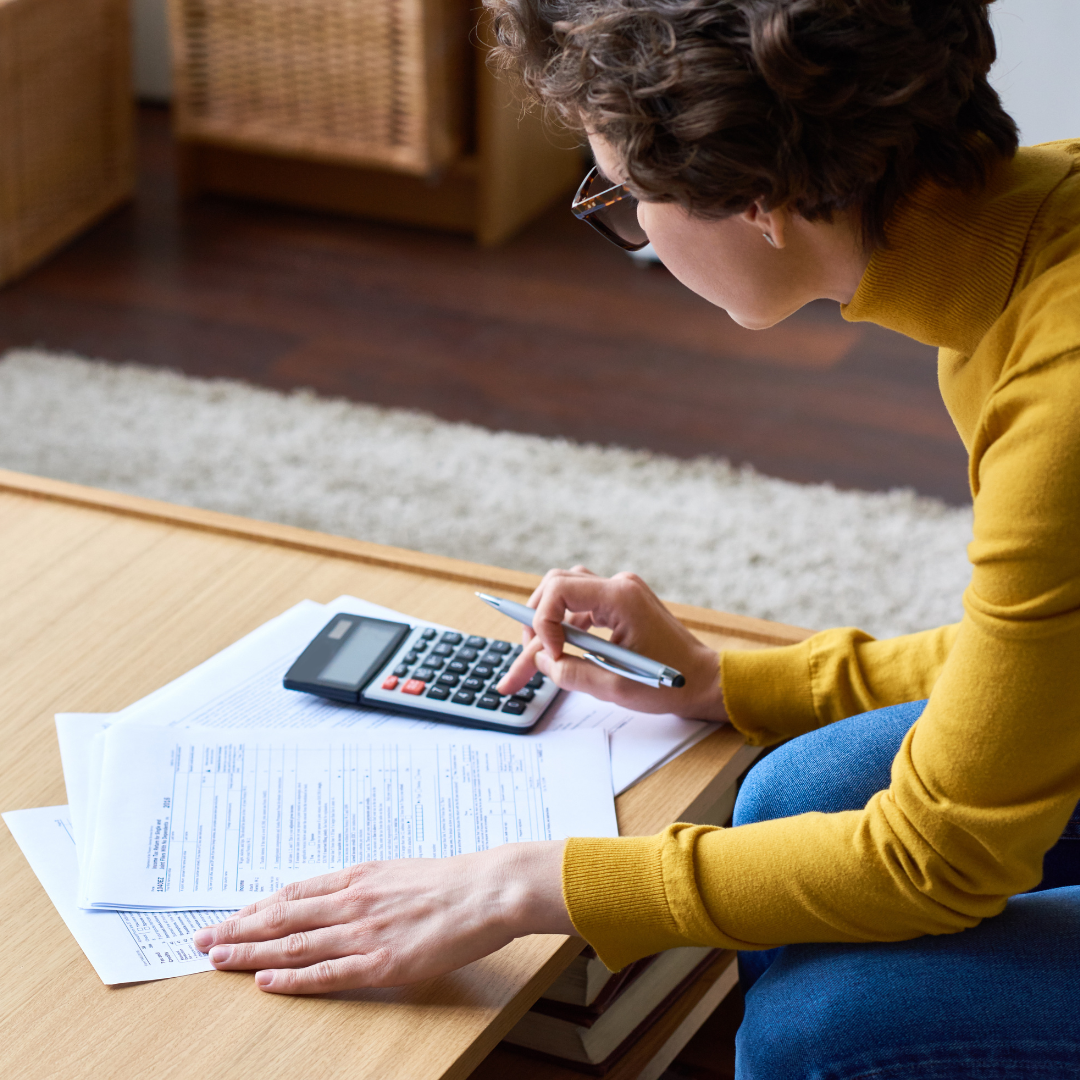

Create a budget

Well, the great thing about budgets is that they are easy to set up and easy to follow. A budget consists of three parts: expenses, income, and savings. In order to make sure your budget is working for you, it is important to track your expenses on a regular basis. You can use a spreadsheet to keep track of your income and expenses or create a budget by hand. Either way, it is important to know how much money you have coming in each month and how much is going out. If you can keep track of your income and expenses, you can make sure your money is going towards the things that are important to you, like saving for a down payment on a home or paying off debt.

Lower your debt

We’ve all been there: you’ve got money in the bank, but you’re still struggling to make ends meet. You’ve got a slow job, and you’re living with roommates; you’re dealing with an illness. Soon enough, you find yourself $1,000 in debt. You can’t control the interest rates on your credit cards, but you can take steps that can help you find a better financial footing.

You have a lot of debt, and it’s taking a chunk out of your budget. You’re stuck in a debt cycle that’s making everything worse. But debt doesn’t have to run your life. If you’re not borrowing money, you have time on your side to find a solution-and no, it doesn’t have to be drastic.

Raise your income

Your budget is only as good as the amount of money you bring in. Increasing your income can be a great way to give your budget the support it needs and handle your expenditure. You could do this by getting a better job with a higher salary, or you could start making money on the side. Some people start a lifestyle business, while others invest in white label sportsbook software and become bookies. There are plenty of ways you can raise your income with little effort. A higher sum every month can also bring down debts faster and help you save more money, which is what we’ll be talking about next.

Save more money

Finding ways to save money is difficult at times, and easy at others. Larger purchases are trickier to find discounts for truthfully, but at the same time smaller shopping sprees could be gained for much less cash out of your pocket. For example, you could look into the best Target skincare products online, find promo codes for them, and then save a lot over a long period of time on these items in particular. This is one example of course, but the concept is the same for anything else.

Conclusion:

You know the problem – you’re tired of your financial situation and think you can do better. You’re ready to make some sacrifices to get out of debt and become a financial success. But how? Well, it’s simple: Cut unnecessary expenses, and add in some extra income to get the money you need – and ditch the debt and then some. And that’s it! To get out of debt, all you have to do is stop spending money you don’t have on things you don’t need and start earning money you do have.